Perverse incentives

that affect the average investor

The stock market can be regarded as a transfer of wealth

mechanism from minority shareholders and investor to company promoters and

managers. What has caught my mind recently is three different examples.

Pershing Square

The first is Pershing Square one of the most high-profile

hedge funds in the world led by its enigmatic CEO and founder William (Bill)

Ackman.

Pershing Square had an impressive track record compounding its

returns between 17.6% - 20.8% p.a. net of fees depending on the structure

between 2004/5 and first half 2014. This performance enabled Pershing Square to

launch a large Listed Investment Company in the Netherlands raising $2.7B USD.

This raising provided Ackman with permanent capital to invest and a guaranteed

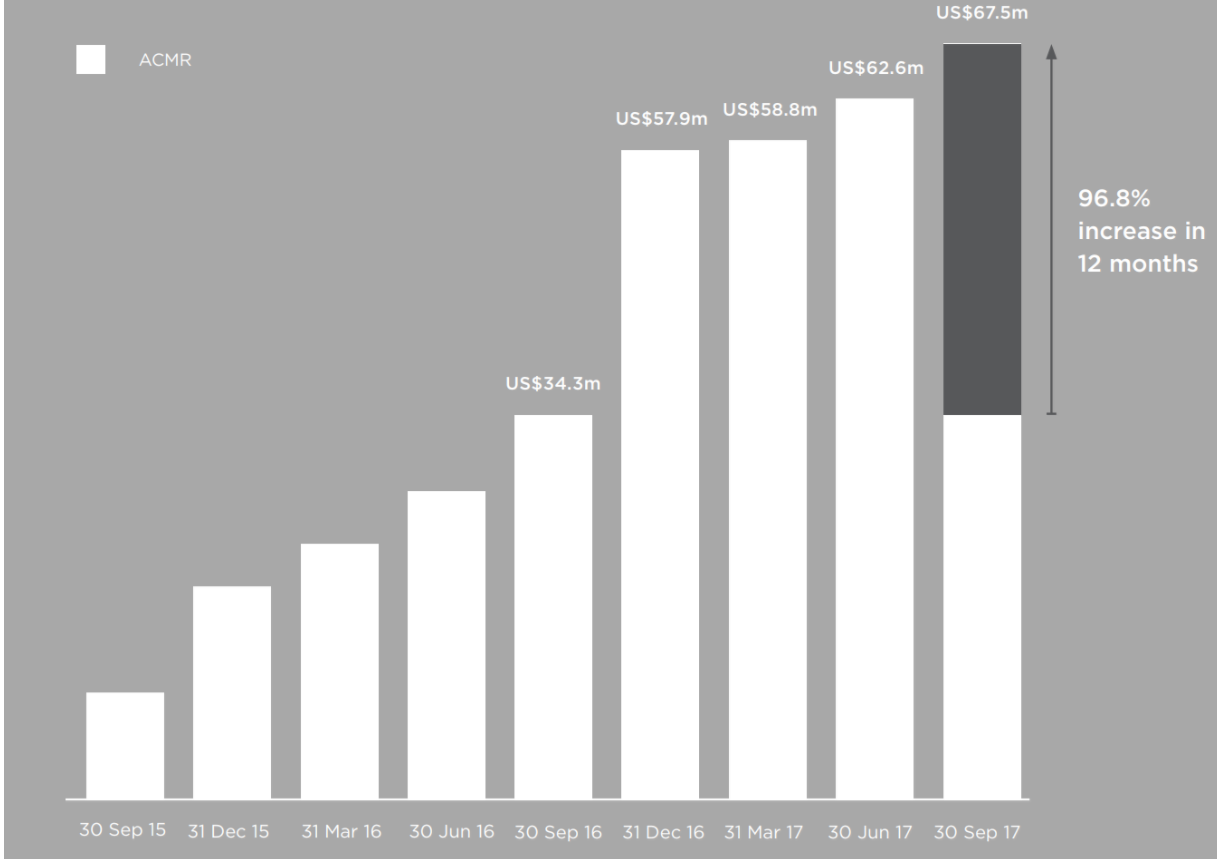

fee income stream. Pershing Square employee numbers also swelled as can be seen

in the graph below.

What precipitated was a series of poor returns from

investments including Valeant, Herbalife and Mondelez. This blog post is not questioning

the merits of these investments but what has subsequently resulted is a significant

amount of lost money. However, Pershing still likes to focus on its long-term

compounding record as Pershing Square. What is more important though is Pershing

Square’s money weighted return. These returns take account of how much $ return

was generated. As Pershing generated most of its positive return when it was

managing relatively smaller; amounts of money and generated negative return

when it was managing larger amounts the money weighted return would be far

lower than its time weighted return.

The other fund management trick that Pershing Square has

pulled is that Bill Ackman has reincarnated himself as a fund manager but conveniently

forgotten his past track record. Previously he was managing Gotham Partners

where the funds shuttered due to redemptions from poor performance.

Investors must be cautious when investors raise large

amounts of money off the back of a historical track record obtained under

different conditions. Many fund managers right now are trying to raise as much permanent

capital as possible as they have strong track records from the bull-market in

equities due to compressed interest rates. Investors should beware the

incentives of the managers behind such actions.

CBL Insurance

CBL recently listed in 2014. It has a great run as a recent

IPO increasing from $1.55 to $4.00. CBL is an insurance company which specialises

in niche insurance predominately in France.

CBL exceeded its prospectus forecasts, however it made a

number of acquisitions which were not forecast in the prospectus forecasts. Adjusting

for these acquisitions CBL still beat prospectus forecasts by $5.2m PBT or

8.2%. However, looking further into the result the FY16 result was aided by a

release of provisions of $5.8m.

This would be fine, however the events that subsequently

followed suggest that the timing of the release reserve to ensure prospectus

forecasts were met was extremely convenient.

In April 17, little over 1 month post the FY16 result was

released 20m shares were sold at $3.26 to NZ and Australian investors. This

realised $65.2m for the Directors and Management. On August 18th CBL

came out with a surprise announcement, shortly before it was due to release its

1H17 results, that it would miss its internal operating profit expectations by

$17.5m due to a $16.5m strengthening of its insurance reserves. This seemed

strange given the reserves were released only 6 months prior. The stock

subsequently fell from $3.75 to a closing low of $2.80. To add salt to the

wounds CBL has recently updated the market again in February 2018 and has

remained suspended from trading as it expects to make a future claims reserve strengthening

adjustment of $100m to the reserves, it will also take a $44m write-down of

receivables arising from SFS, a business that it acquired in 2016.

The observation is in businesses where significant accounting

adjustments can be made which significantly affect the profitability of the

business such as finance and insurance companies in situations where management

have an incentive to produce a favourable result it is necessary to exercise

increasing skepticism towards the results produced.

ITL Healthcare

ITL healthcare conducted a suspicious share buy-back which

was announced on the 25th of October. The company began buying back

shares at 40.5c and purchased aggressively right up to December 29. Prior to

this buy-back the previous buyback was conducted at less than half the price

being 20c on 8 February 2016.

ITL purchased 4.11m shares in November at prices between

0.40 to 0.47 which was 72.5% of all volume traded in that month.

ITL purchased 7.99m shares in December at prices between

0.415 to 0.475 which was 71.3% of all volume traded in that month. The volume

that wasn’t bought by ITL consisted of two director sales, conveniently at the

high share-price of the month of 0.47. Andrew Turnbull sold 990,000 shares and William

Mobbs sold 2,343,543 shares. Adjusting for these director sales ITL purchased

100% of all shares during the month and effectively pushed the share-price to a

level that allowed the directors to sell down. The buy-back has now stopped and

the share-price has fallen 22%.