Pushpay - Does it deserve its valuation

Pushpay is currently

valued at $1.15 billion New Zealand dollars with a share-price of $4.21 at 28

December 2017.

I find this valuation

hard to justify for a number of reasons.

Revenue is overstated

Firstly the gross

revenue number that the company's provides needs to be adjusted for the third

party payment processing fees . Transaction fees amounted to 43% of operating

revenue. While it is easy to make this adjustment many investors will value PPH

like other Sass companies on an Enterprise value to gross revenue multiple

which overvalues PPH compared to peers.

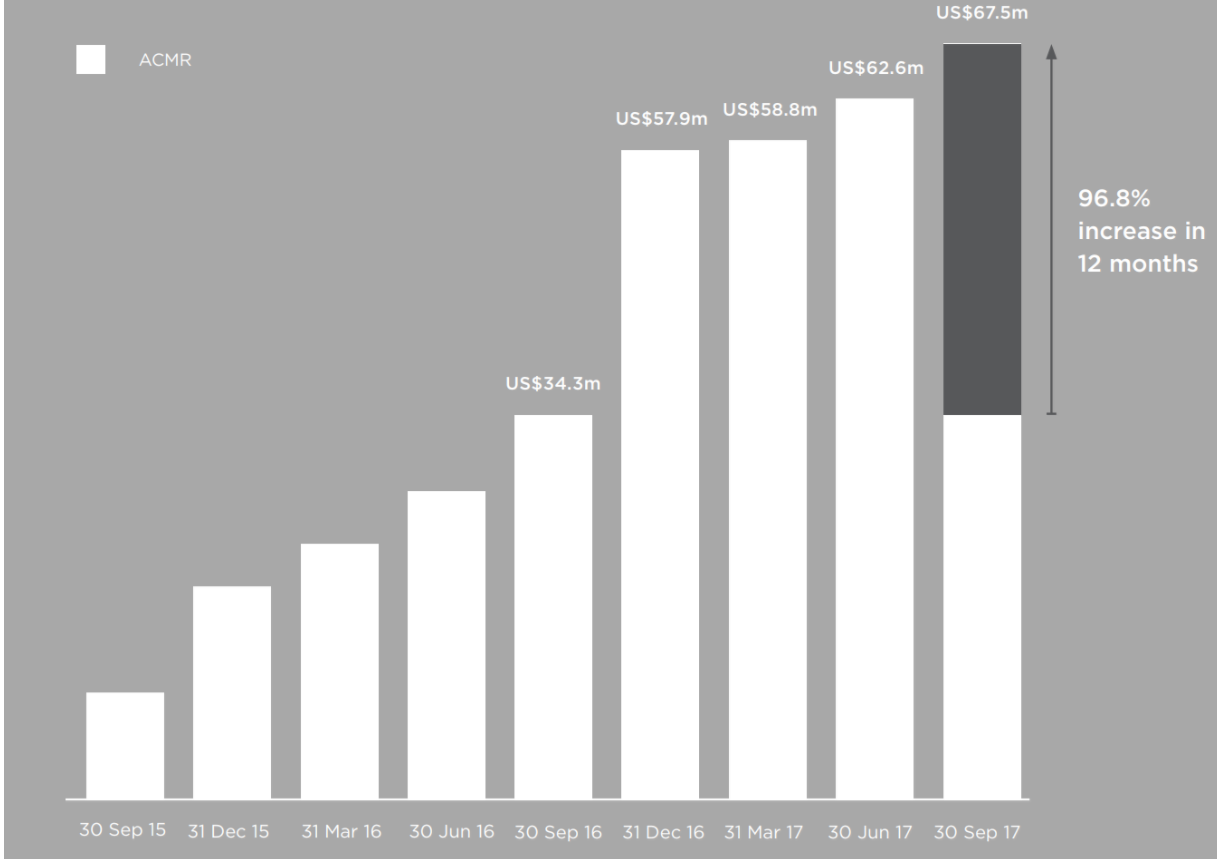

Annualised Committed

Monthly Revenue (ACMR) – is not actually committed

Annualised Committed

Monthly Revenue (ACMR) – is defined as monthly Average Revenue Per Customer

(ARPC) multiplied by total Customers and annualised. It consists of

subscription fees which are recurring and can vary based on the size of the

Customer and Volume Fees which are a variable fee income generated from payment

transaction volume (in the case of the faith sector, this is usually a

percentage of total donations).

CAC is understated

The total sales and

marketing, and customer success costs over the six months ended 30 September

2017 were $16.7 million, contributing to an ACMR increase of $33.2 million.

This is misleading as

the ACMR increase relates to a 12-month period whereas the sales and marketing

costs relate to the most recent six month period. In this same 6 month period

to 30 September 17 ACMR only increased by $8.7m. This is a CAC of $16.7 / $8.7

= 1.9x or 23 months rather than the less than 12 months they are quoting.

If we then take the

gross margins of 57% then it is $16.7 / $5m (57% x $8.7) = 3.34 years.

Subscription revenue is likely to be very high (only hosting costs) but the

transaction volume revenue is much lower GM of 38% ($12.3m cost and $19.8m

revenue)

LTV indeterminate

Low switching costs

and limited customer history is difficult to conclude customer retention will

hold at 95% for the long run. For example it implies that on average a customer

will stay with PPPH for 20 years, however most customers have been on the platform

for < 18 months to date. This is why I don't think we can put much

reliability on the lifetime value calculations. An analogy is a finance company

that has the majority of its book as fresh debt on its books it is not likely

to record high bad debts until the debt becomes more seasoned and the borrowers

get into trouble.

Fee pressure

There is likely to be

fee pressure on the volume fees charged. Other competitors in the market have

lower transaction fees than the standard price: 2.9% + 30 cents per

credit/debit card transaction while not charging any subscription fees.

Processing revenue was

$19.8m for 6 months to 30 September 2017, if we assume an average payment fee of

2.9% as disclosed on their website this would assume payment volume was

($19.8m/2.9%) = $683m for 6 month period and it is now annualising $2.1B.

It is unlikely that

the 2.9% payment fee is the realised rate due to discounts given. We can prove

this by taking $2.1B x 2.9% = $60.9m revenue and the subscription revenue for 6

months was $10.8m for 6 months or at least $21.6m annualised. Therefore total

ACMR should have been at least $82.5m whereas it was $67.5m.

To calculate the ACMR

for subscription revenue when can use the average number of customers in 1H18

which was (6737+7121)/2 = 6929. This results in an average subscription revenue

of $3117 ($21.6m/6929). So the annualised subscription revenue at 30 September 17

would be 7121 x $3117 = $22.2m. Therefore the payment volume revenue would be

$67.5 - $22.2m = $45.3m. Taking the $2.2B run-rate of payment volume the bp

would; be 2.06% ($45.3m/2.2B) rather than the 2.9% quoted rate. I think this is

a number that PPH don’t want disclosed as I would assume it is likely to fall

over time as increased competition puts pressure on margins.

What will PPH earn if

they reach their goals

In 2016, $123 billion

was given to religious organisations in the US and PPH process just under 2% of

that currently. PPH state their goal is to reach the milestone of $10B in

Annualised Monthly Payment Transaction Volume. PPH does not give a timeframe

but this is 4.55x greater than the $2.2B annualised payment transaction volume

at 30 September 2017. The ACMR was $67.5m, the breakdown between subscription

revenue and transaction revenue is not stated by the company.

If PPH was to get to

$10B of volumes this means $206m of revenue. With a GM of 38% = $78m GP.

Subscription revenue is harder to forecast as it won't be 4.55x larger as

payment volume will benefit from increased take-up from existing customers.

I am making an

estimate that half of the growth in volume comes from new clients that will pay

for more subscriptions and the other half will be from current customers that

won't necessarily need to pay higher subscription revenue. This will mean that

subscription revenue would increase by 2.27x (50% of the 4.55x) to $50m

(2.27x$22.2). Lets assume this is at 100% GM (aggressive) so $50m GM.

In total $128m GP

could be achievable at $10B of payments. Operating expenses were $29.9m for 6

months to 30 September 17 so doubling that would be $60m (it is likely operating

cost will be much higher if transaction volume is 4.5x higher though). This

results in a PBT of $68m and using the new US corporate tax rate of 21% (could

be higher) a NPAT of ~$54m. This is a PER of 22x earnings. I’ll let you decide

whether you are comfortable paying 21x earnings given this scenario is good

risk/reward.

Where could we be

wrong

a.

PPH are indicating

they will be at $100m ACRM by 31 December 17. THis is a large jump from 30

September 17 where ACMR was $67.5m so if it is achievable that will very high

sales result and produce a low CAC. This is possible given there was a large

jump last year in the December quarter.

b.

Transaction fee

margins may decline further. It is hard to see how the improve.

c.

Operating expenses may

increase at a faster rate. IT is hard to see them falling however they may do

so if marketing spend is pulled back.

d.

The $10B of

transaction volume may prove to be conservative given the market size of $123B.

e.

Subscription revenue

may increase faster than what we expect and may be at a higher run-rate than

$50m by the time the company is at $10B of payments.

f.

Tax rate is much

different to 21%. PPH will have tax losses to shelter income for some time as

well.

No comments:

Post a Comment