How do tax rates impact the long-term compounding nature of equities 2 July 2017

There has been a significant amount of analysis on what makes a business a good compounder of capital however one of the most important factors is the tax rate the company must pay.

Companies that pay a low amount of tax will compound capital much faster than companies that pay a higher portion of the earnings in tax. There are ways in which companies in high tax jurisdictions can minimise their level of tax paid by structuring their tax tax affairs however this will often come with associated negative consequences. For example US corporations being unable to repatriate their offshore profits back to the United States as this will trigger a tax liability in the US.

It is easier for some types of companies to structure their taxi affairs than others. Companies that have a high amount of intellectual property or intangible assets can more easily shift those assets offshore to low tax jurisdictions compared to companies that have a high amount of tangible assets which are more difficult to shift

The WalletHub broke down the overall tax rate for the S&P 100 in 2015 using the companies' annual reports. As opposed to the supposed 35% federal statutory corporate tax rate in the US, these companies paid an average rate around 28% for the year, including federal, state, and international taxes.

There come quite often be a difference between the tax expense reported in the financial statements and the actual corporate tax paid due to deferred taxation such as using accelerated depreciation rates for tax purposes.

In the case of Berkshire Hathaway (BH), much of the difference comes from faster depreciation for tax purposes.

WalletHub has BH with a rate of 30.1%. Going to the BH 2015 K-1 (page 68) we find "Earnings before income tax" of $34.946 billion and "Income tax expense" of $10.532 billion, which is 30.1%. The amount paid which you will find on page 87 was $4.535, which is just 13.0% of pretax income.

In the case of BH, much of the difference comes from faster depreciation for tax purposes. Berkshire's net deferred tax liability grew by $1.263 billion. And as long as the company continues to put more property in service, at least on a dollar basis, than it retires that deferred tax liability, currently $63.199 billion will likely continue to grow.

Many European countries have taken their approach to have low corporate income tax rates but high value added tax or consumption taxes.

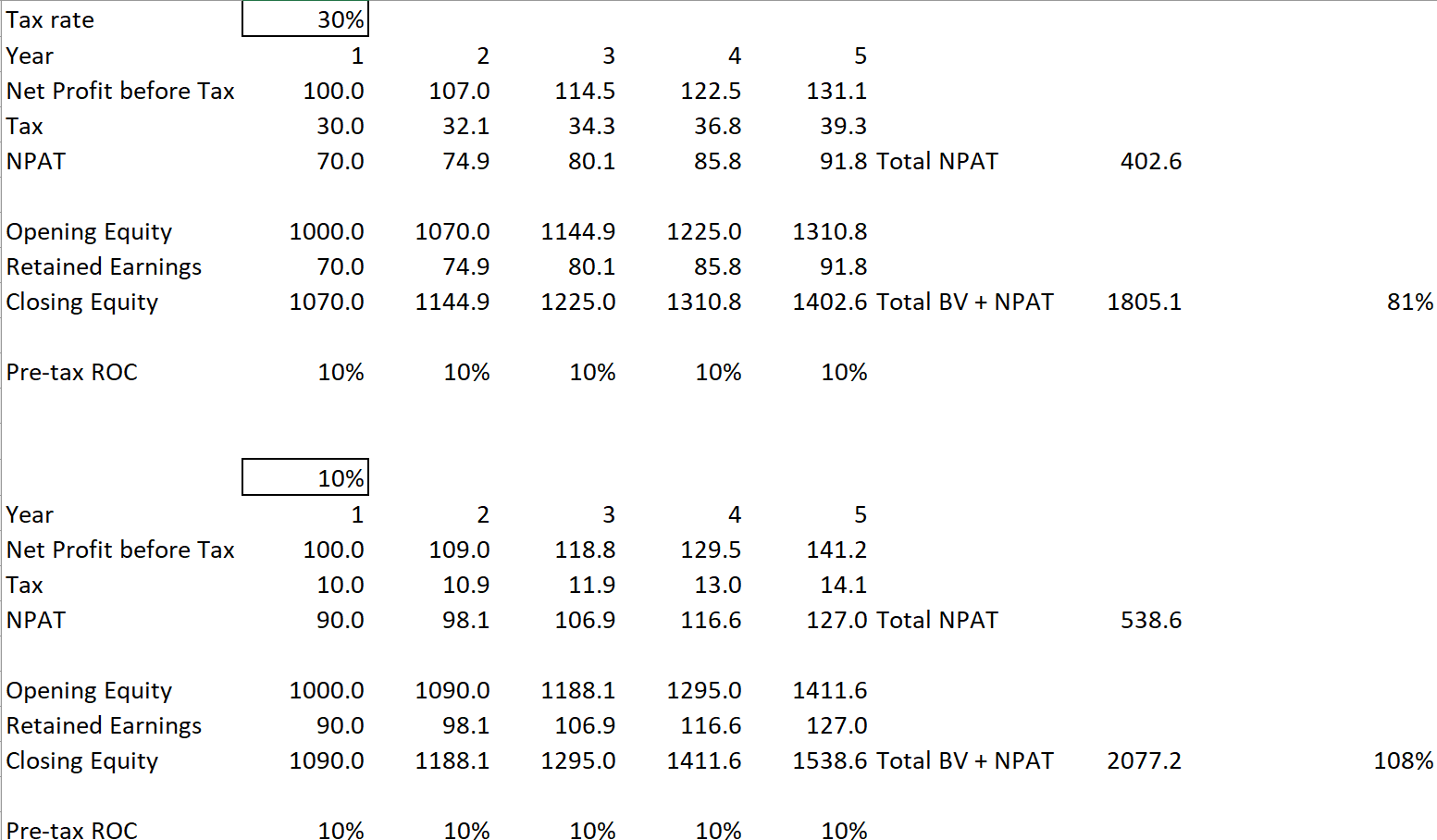

An example of the compounding nature of lower taxes can be seen in the example below.

This would be the equivalent of a company that is based in Australia and paying 30% corporate taxes versus a company based in Bulgaria and paying 10% corporate tax rate. The total return assuming that company was purchased at a book value of 1 times and is still trading it 1 times book value after 5 years is 81% for the company in Australia compared to 108% for the company in Bulgaria.

Conclusions

Investors should pay more attention to the after tax returns companies are generating and also the after tax returns attributable to themselves. Taxes at a personal level should also aim to be minimised by investing through tax efficient structures and residing where possible in lower tax jurisdictions.